Warsh on Top; Commodities on the Mat

March 6, 2026

Fed politics hit the narrative; the dollar firmed, real rates backed up, and metals unwound sharply.

January was supposed to be a back to normal month: a steady Federal Reserve, a predictable FOMC meeting, and markets rotating back to the usual growth, inflation, and data rhythm. Instead, the month ended with the tape dominated by a different variable: institutional risk. That single shift was enough to flip crowded positioning across commodities into a fast, messy unwind.

The sequence mattered.

1. The January FOMC: steady policy, not a dovish pivot

The Fed held the target range at 3.50% to 3.75%1. The messaging was consistent with a cautious committee: inflation still not fully solved, growth not collapsing, and no urgency to move quickly. Markets did not get a clean green light for aggressive easing expectations. The meeting validated a wait and see stance rather than delivering a pivot. That is why the meeting itself was not the shock. The shock was what followed

2. The Warsh effect: a regime narrative enters the price action.

When the Warsh nomination hit, investors did not need a detailed policy blueprint to react. They needed a plausible story that could be traded immediately:

- Higher for longer becomes a more credible baseline, or at least a more tradable one.

- Balance sheet restraint becomes more plausible in the market imagination.

- Fed independence and governance become a live macro input rather than background noise.

That mix matters because markets price not only the expected path of rates, but also the confidence band around that path. When governance headlines rise, the distribution of outcomes widens. Volatility premia rise. Term premium can reprice. The dollar can become more sensitive to headlines.

3. Why commodities got hit: the three part mechanism

Part A: The classic macro headwind

A firmer dollar and higher real rates are a direct headwind for precious metals. If the market concludes that policy tolerance for inflation is lower, or that financial conditions will stay tighter, the knee jerk reaction tends to be stronger USD and higher real yields. That is a tough backdrop for metals that do not yield.

Part B: Positioning was already stretched

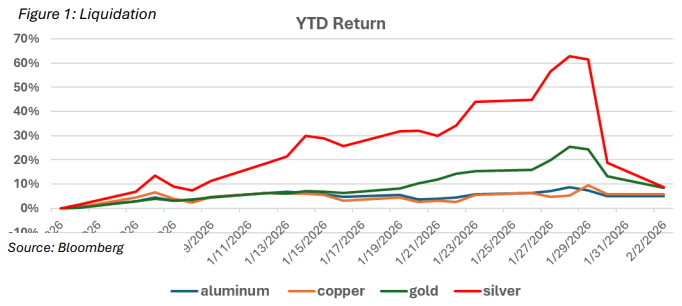

The commodity complex had strong momentum and a widely shared bullish narrative. When a trade becomes crowded, the reversal is rarely orderly. Early selling turns into profit taking, then into risk reduction, then into liquidation (Figure 1).

Part C: Leverage and mechanics turned a pullback into a flush2

Once metals started sliding, the plumbing took over. CME raised margin requirements on metals after the plunge, which is forcing leveraged players to liquidate into weakness and amplify downside moves. This is how you get a mat moment: the move becomes mechanical.

4. Why silver looked especially ugly

Silver often behaves like a hybrid. It can trade like a monetary metal when the narrative is debasement or inflation hedging, but it can also trade like a high beta commodity when the tape turns risk off. That combination makes it prone to overshooting in both directions.

In an unwind driven by stronger USD, higher real rates, and forced deleveraging, silver can fall faster than gold because it is frequently used as a higher octane way to express the same theme.

5. What this means going forward

The key takeaway is that governance risk has joined the macro watch list. Even if the Fed remains data driven in practice, the market will treat leadership headlines as an input into policy credibility, communication discipline, and balance sheet preferences. For cross asset behavior, that tends to raise correlations in headline windows. When the driver is regime repricing, assets that usually diversify can suddenly trade together until the tape finds a new equilibrium.

6. What I am watching next

- Reaction function : Is the Fed more focused on sticky inflation or on protecting growth and jobs

- Credibility and independence : Do leadership and governance headlines widen the risk premium investors demand

- Balance sheet and liquidity : Does the market start pricing a smaller balance sheet and tighter liquidity conditions

- Volatility regime : Do we settle back into low vol or stay in a headline driven, higher vol environment

January did not end with a simple story about one data point or one meeting. It ended with a reminder that markets price regime, not just rates. And when that regime narrative shifts, crowded trades do not walk out. They get carried out.

1https://www.federalreserve.gov/newsevents/speeches.htm

2https://www.cnbc.com/2026/01/30/silver-gold-fall-price-usd-dollar-fed-warsh-chair-trump-metals.html

↑ Back to top