The Barrell, the Battlefield, and the Portfolio

March 19, 2026

What an oil shock really does to markets

Markets sometimes tell you, faster than the headlines do, when a geopolitical event has crossed into macro territory. This looks like one of those moments. Oil is higher, equities are softer, and bonds have not delivered the clean offset investors usually expect in a classic risk-off move. That combination matters because it suggests the market is not treating the conflict as a contained shock. It is pricing a broader inflation and policy problem.

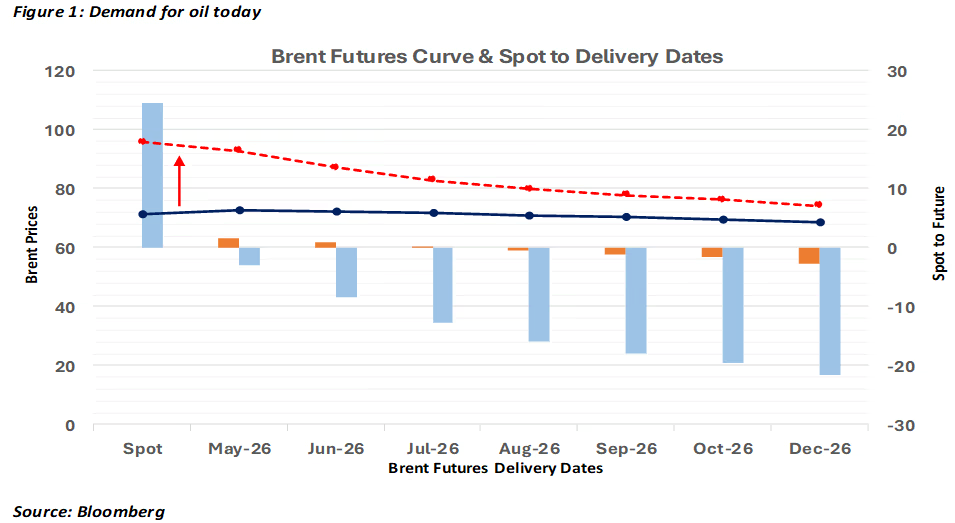

The move in crude is central to that repricing. The issue is not simply that oil has risen. The issue is that markets are reacting to the possibility that one of the world’s key energy arteries could become materially less reliable. When the risk centers on a chokepoint as important as the Strait of Hormuz, the market stops thinking about geopolitics in the abstract and starts thinking about physical supply, freight, inflation, and policy transmission.

In quieter periods, investors can usually look through conflict. They assume production continues, shipping adjusts, and any price spike fades before it does lasting macro damage. That is not the framework now. The current move suggests investors are assigning a higher probability to disruption that lasts long enough to affect pricing behavior well beyond the energy complex (Figure 1).

That is the key transmission channel. Oil does not stay in oil. It feeds into headline inflation, transportation costs, industrial input prices, consumer psychology, and ultimately central-bank reaction functions. Once that process starts, the market is no longer pricing a regional event. It is pricing a macro shock with cross-asset consequences.

The cross-asset response already reflects that shift. In a straightforward growth scare, equities weaken and government bonds rally. Here, that relationship has been less reliable. Yields have remained under pressure because higher energy prices complicate the disinflation story and reduce confidence that central banks can respond aggressively if growth softens. That is a more difficult regime for portfolios because the usual diversification channels work less cleanly.

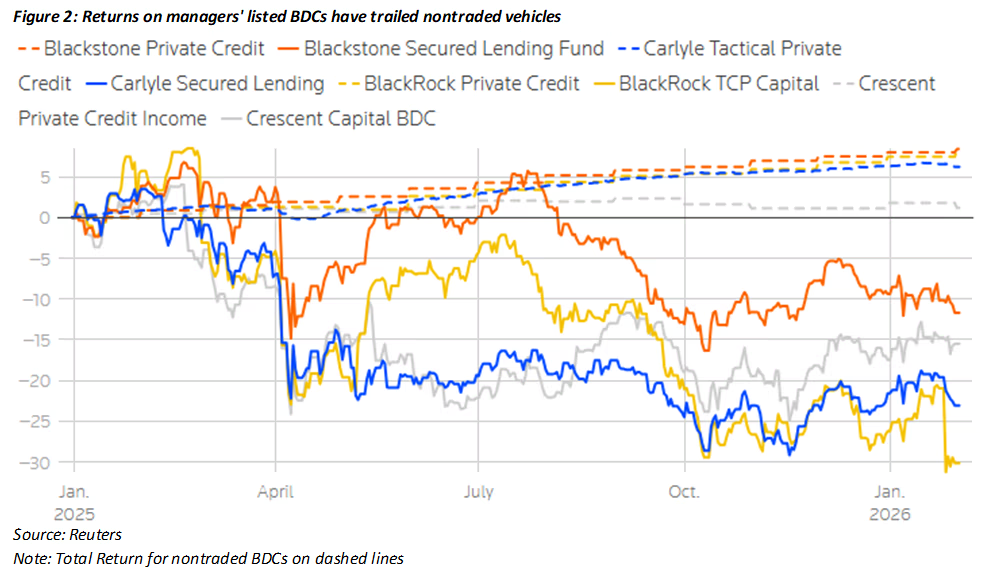

Credit is starting to echo the same message. Public credit tends to show stress first through softer demand for new deals, weaker risk appetite, and a gradual widening in spreads. Private credit is different. The issue there is not just credit quality. It is also confidence in marks, liquidity terms, and the ability of vehicles to refinance and support themselves if conditions tighten.1

That is why the recent pressure matters. Investors are paying closer attention to discounts to stated value, redemption friction, and refinancing needs across business development companies and adjacent private-credit vehicles (Figure 2). That does not automatically imply a break, but it does shift the market from a yield discussion to a credibility discussion. In private markets, that change in framing can matter as much as a move in default rates.

My takeaway is simple: private credit is most vulnerable when investors begin asking not what the portfolio should be worth, but what it could be monetized for, on what timeline, and with how much balance-sheet support behind it. Once those questions move to the center, valuation, liquidity, and funding risk stop being separate issues and start reinforcing one another.

That matters beyond private credit itself because the broader market is trying to price two related ideas at once. First, an oil shock can keep inflation firmer than expected. Second, tighter financial conditions can expose structures that looked stable only because capital was abundant and exits were orderly. Put differently, this is not just an energy story. It is a stress-test for valuation discipline and liquidity assumptions across risk assets.

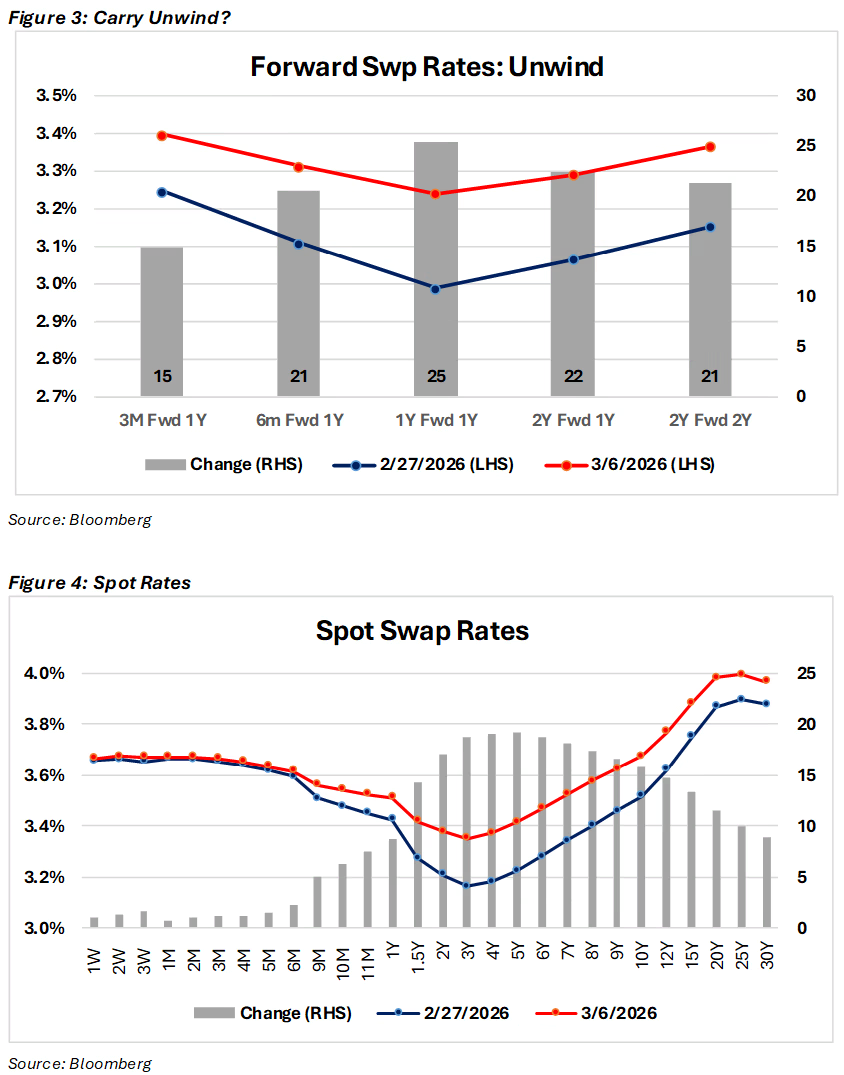

For the Federal Reserve, that is the uncomfortable part. A normal growth scare would pull the market toward easier policy. An energy shock works in the opposite direction by pushing inflation risk back up. That does not mean the Fed has to tighten into weakness. It does mean the bar for a market-friendly easing response becomes higher if oil is feeding directly into inflation expectations (Figure 3 & 4: Carry Trade Unwind).

That leaves investors in a more difficult allocation environment. Equities face margin pressure and softer demand. Bonds face the risk that inflation proves sticky enough to keep yields elevated. Public credit faces tighter financial conditions. Private credit faces the same pressures, plus the additional challenge of opaque marks and constrained liquidity. When those forces hit together, portfolio construction gets harder precisely when diversification is most needed.

The broader lesson is that markets are not reacting to war in the abstract. They are reacting to the channels through which war changes pricing. Oil is the clearest channel because it moves directly into inflation, policy expectations, and risk appetite. Credit is the second channel because it reveals where confidence, leverage, and liquidity are most exposed. That is why this episode deserves to be treated as a macro event, not a geopolitical side story.

Investors do not need to assume the worst-case outcome to take that seriously. They only need to recognize that once the barrel begins driving the rest of the portfolio, the battlefield is no longer remote. It is already embedded in the market regime.

↑ Back to top

↑ Back to top